Federal Budget 2026-27 Overview

This budget fundamentally changes how capital gains and trusts are taxed by introducing a 30% minimum tax rate and many other changes.

If you think you/accountants are already busy, then this budget will increase your/their workload dramatically. With changes to the capital gains tax (CGT) discount, pre-CGT assets becoming subject to CGT, negative gearing, trust distributions, the reintroduction of loss carry back rules, making the instant asset write-off permanent and changes to the fringe benefits tax (FBT) exemption for electric vehicles, accountants Australia-wide will be inundated with calls from clients wanting to know how this budget will impact them – with 1 July 2027 and 1 July 2028 becoming key dates.

This budget fundamentally changes how capital and trusts are taxed in Australia. With 30% minimum tax rates for capital gains and trusts, there will be significant changes to how investments are selected and structured.

Some of these changes may commence after the next Federal election, so may become contested policy settings.

Below are the key tax highlights. Keep an eye out for further articles which delve into each topic in greater detail and will be updated as CA ANZ has discussions with key political advisers and Treasury over the next few days. There will also be articles outlining the numerous other changes that were made in this bumper budget.

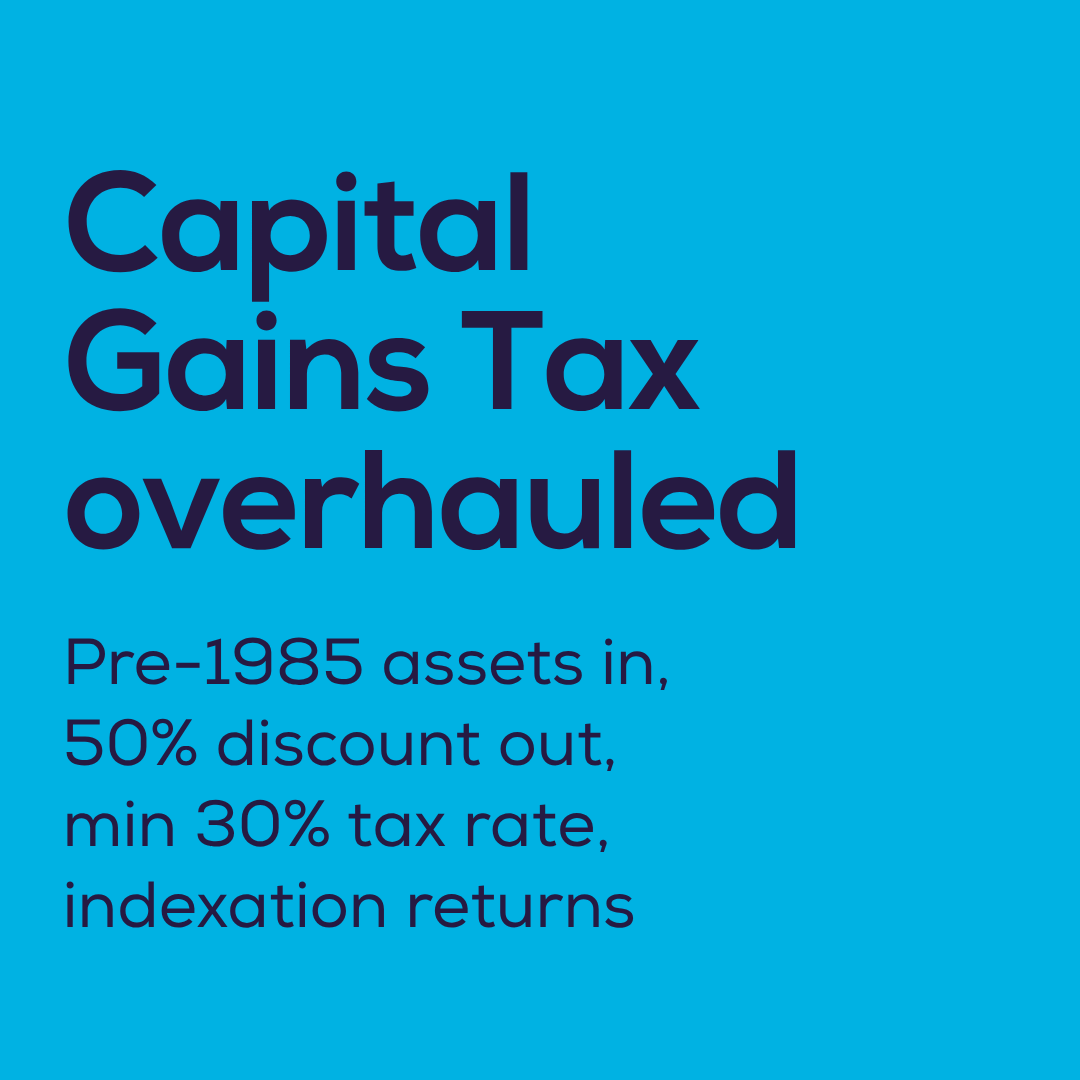

Pre-CGT assets

The best kept budget secret was the plan to bring pre-20 September 1985 assets (pre-CGT assets) into the CGT system. Gains made by these assets from 1 July 2027 will be subject to CGT. Owners of such assets have the choice of selling before 1 July 2027 to crystalise an untaxed gain or to obtain a market valuation of the asset at 1 July 2027 to ensure that there is documentation of how much of the future realised gain is post 1 July 2027.

Capital gains taxed at 30%

Another well-kept budget secret is that there will be a minimum 30% tax on net capital gains from 1 July 2027. This reduces the benefit of deferring the capital gains realisation until a later time when a taxpayer has a lower marginal tax rate.

Capital gains tax (CGT) discount

From 1 July 2027 the 50% CGT discount on capital gains will be replaced with indexation of the cost base. The 50% CGT discount will continue to apply to gains made before 1 July 2027.

However, investors in new residential properties will be able to choose between the 50% discount on a capital gain or indexation of the cost base. It is unclear when the purchase needs to have been made.

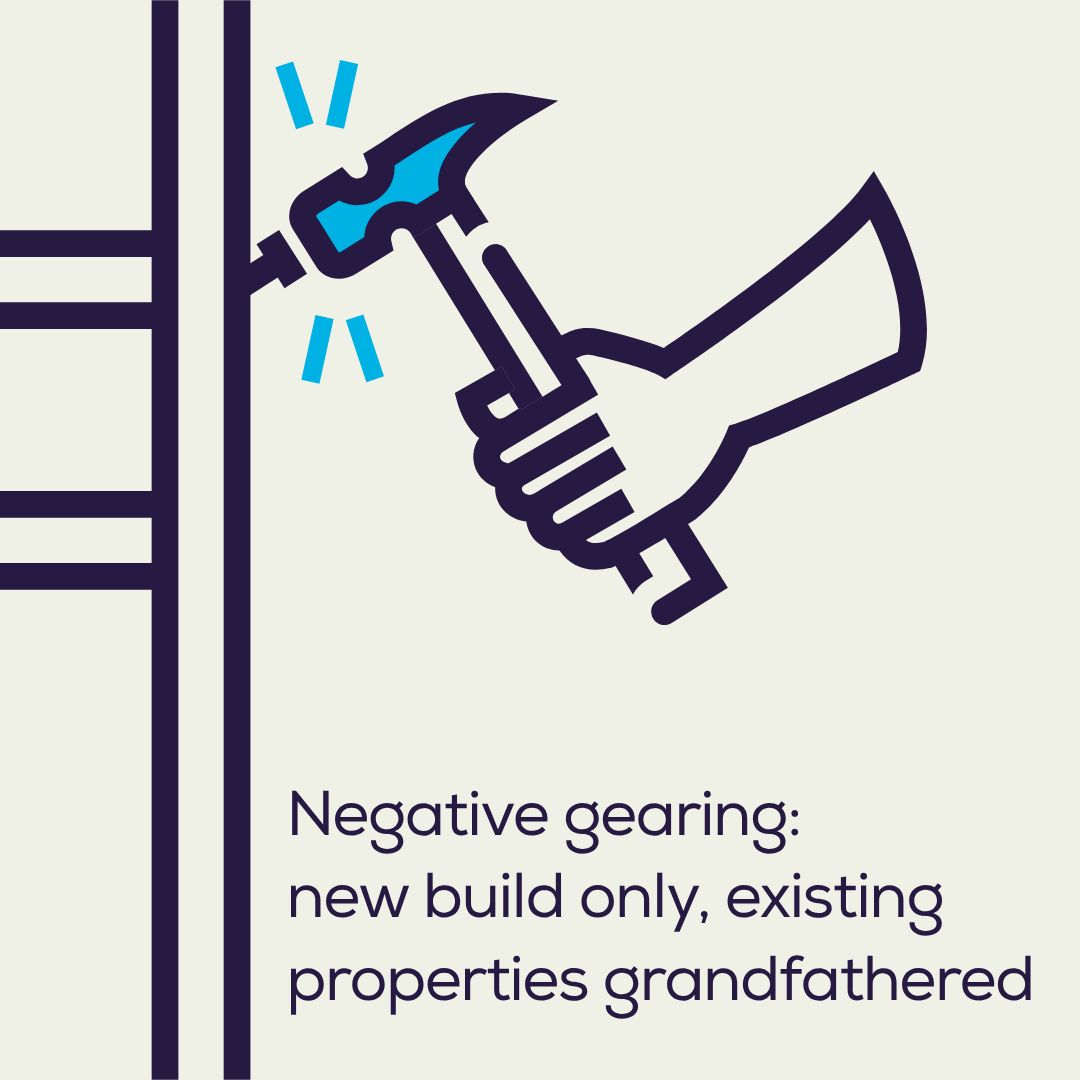

Negative gearing

From 1 July 2027, negative gearing will be restricted to new builds.

Those who intend to buy negatively geared established real estate will only be able to use the losses from negative gearing against rental income or capital gains from residential properties – effectively quarantining these losses to income of the same type. Excess losses will be able to be carried forward.

Those who currently have negatively geared properties (or have entered into contracts but have not yet settled) will be able to continue to negatively gear the properties until they are sold.

Properties purchased between announcement and 30 June 2027 may be negatively geared during this period, but not from 1 July 2027.

Trust distributions

Trusts will have another set of rules to comply with. A 30% minimum distribution tax will apply to distributions made after 1 July 2028. This tax will be collected and remitted by the trustee and will generate a non-refundable tax credit in the hands of certain beneficiaries.

Not all trusts are caught – fixed trusts, widely held trusts, special disability funds and fixed testamentary trusts, complying superannuation funds, deceased estates and charitable trusts are specifically excluded from this announcement.

Not all trust income is captured either. Primary production income, amounts to which non-resident withhold tax applies, certain income relating to vulnerable minors and income from assets of a discretionary testamentary trust that exist at 12 May 2026 (budget day) will not be subject to the 30% minimum tax.

To encourage trusts to be restructured as companies or fixed trusts, new temporary rollover relief will be available for three years from 1 July 2027.

This announcement will require reconsideration of what and how amounts are distributed from a discretionary trust. Beneficiaries whose non-trust income is greater than $45,000 face a 30% marginal tax rate and are largely unaffected by this measure. Beneficiaries whose non-trust income is less than $45,000 may look to receive compensation in the form of salary and wages (if the trust is carrying on a business) to ensure that they do not lose the benefit of the tax-free threshold and the lowest marginal tax rate.

Instant asset write-off

The instant asset write-off has been made permanent. Small businesses (those with less than $10M turnover) now have ongoing certainty that they can immediately write-off depreciating assets costing $20,000 or less.

Loss carry back

To help support growing businesses, the government will permanently reintroduce the loss carry back provisions for companies. Broadly, if a company has been profitable in the past and has paid tax during the past two years, then it can receive the previous tax paid as cash to help it through difficult times. The amount of tax paid back is limited by the amount in the company’s franking account balance. This measure will apply from 1 July 2026 to companies with an annual global turnover of less than $1B.

From 1 July 2028, a new loss carry back provision will be introduced for startups with an annual turnover of less than $10M. During the first two years of operating, it will allow startups that are in losses to claim back a refundable tax offset up to the amount of FBT and pay-as-you-go withholding (PAYGW) that the company has paid in relation to Australian employees.

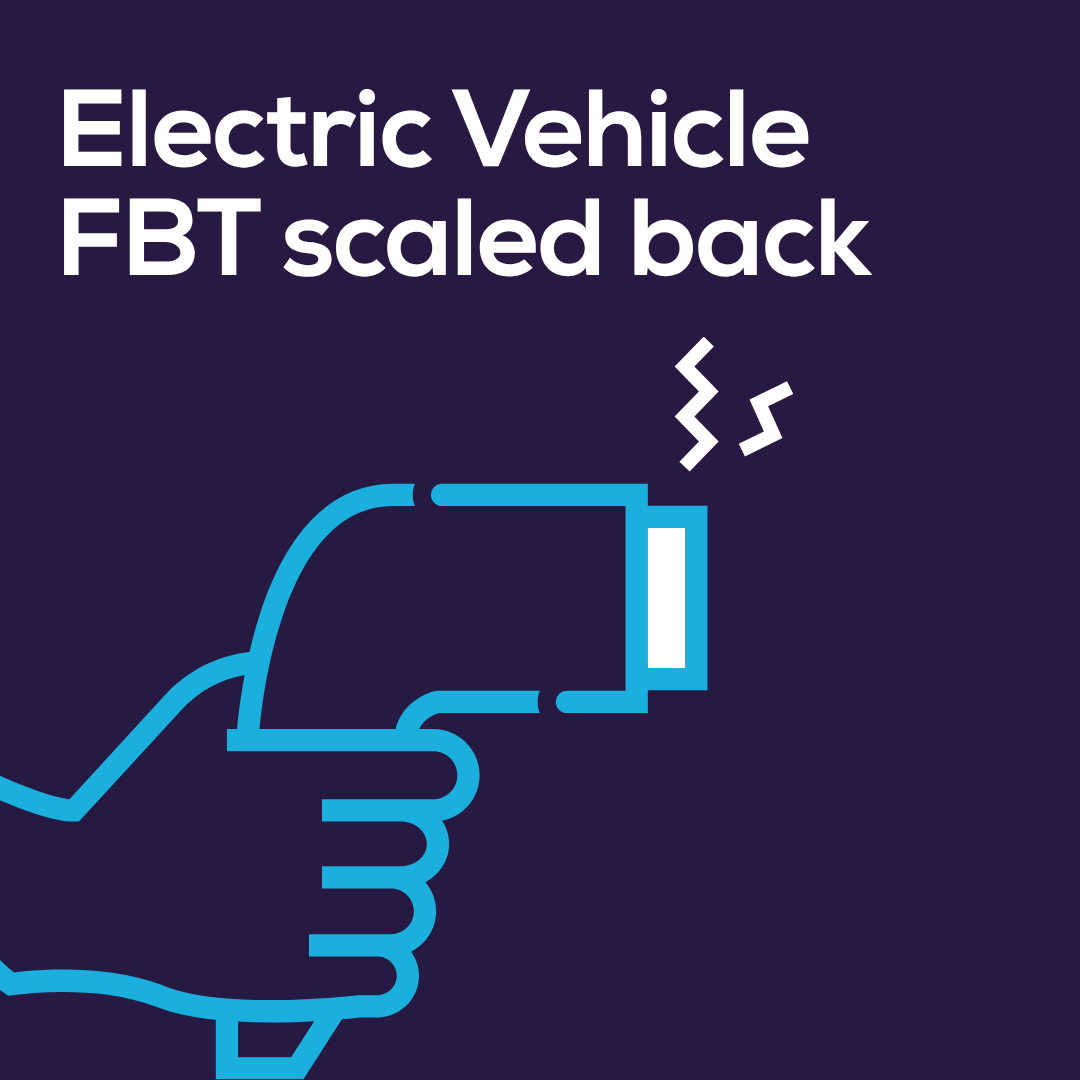

Electric Vehicles and Fringe Benefits Tax

The FBT exemption for electric vehicles (EVs) is being phased out. Existing novated leases are not affected by the changes. Until 1 April 2029, new novated leases of electric vehicles that cost $75,000 or less can continue to access the FBT exemption. After that date the FBT exemption for EVs will not be available.

However, EVs that are under the luxury car limit will still receive some concessional treatment with a permanent 25% discount on FBT which will be implemented through a 15% in the FBT statutory formula. However, reportable fringe benefits will be reported as if the 20% FBT statutory formula or cost base method applied.

Personal tax rates and the standard deduction

The budget reannounces the legislated reduction of the lowest marginal tax rate from 16% to 15% from 1 July 2026, saving a maximum of $268 a year, or $5 a week – around the price of a cup of coffee. As previously announced and legislated, this will further reduce to 14% from 1 July 2027.

The $1,000 standard deduction election announcement from 2025 that has been released as an exposure draft but has not yet been put before Parliament applies for the 2026/27 financial year onwards. CA ANZ’s submission calls for changes to the draft legislation to ensure that the $1,000 standard deduction operates as intended, as a choice.

$250 earned tax offset

What is new is a permanent $250 earned tax offset from the 2027/28 year. Unlike the standard deduction, this offset will be available to sole traders as well as employees.

Return to Federal Budget Coverage

Equipping you with the information and commentary you need to know about the Federal Budget.

Read more