Federal Budget 2025-26 Overview

Approaching an election, the 2025-26 budget provides tax cuts and cheaper beer but little in way of substantive tax announcements apart from more money for ATO compliance. But reform of tax agent regulation continues.

Tax cuts and cheaper beer, you know it is time for an election. The budget provides little relief for tax agents who are struggling with red tape and an uncertain tax system – most announced but unenacted measures remain unaddressed. Instead, there will be significant consultations about the range of sanctions that the Tax Practitioners Board (TPB) can impose on tax agents, the registration requirements for tax agents and compliance funding for the TPB – some of which welcome and others which need careful development.

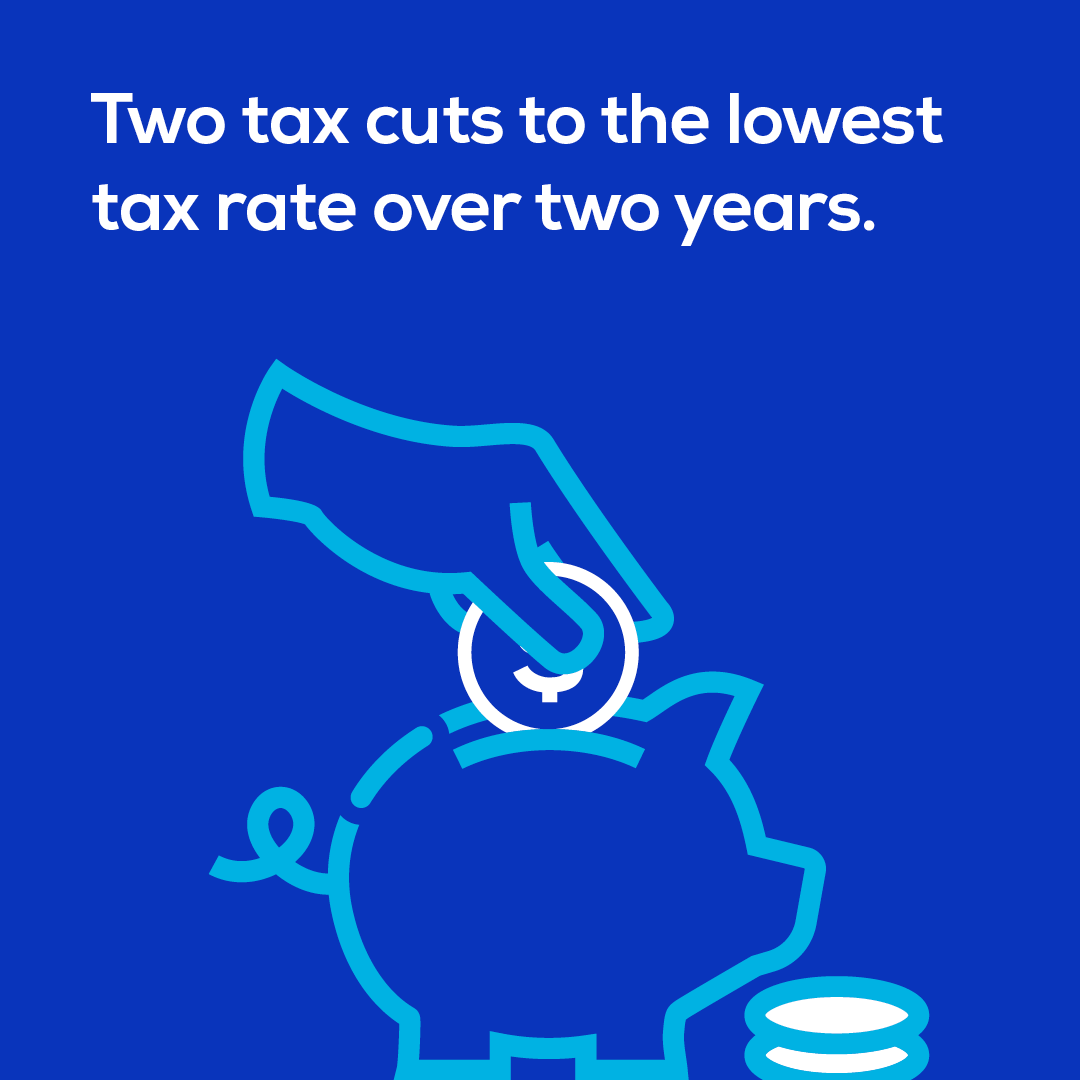

Tax cuts and cheaper beer

In an election year, tax cuts have been announced. From 1 July 2026 the lowest tax rate will be reduced from 16% to 15% and then further reduced to 14% from 1 July 2027, saving taxpayers up to $268 in the 2026/7 year and $536 in the 2027-28 financial year.

In addition, the Medicare low-income threshold will be increased from 1 July 2024 – for singles from $26K to $27,222, and for families from $43,846 to $45,907.

The other major cost of living relief is energy bill relief - $150 for households.

Indexation on draught beer excise will be paused for 2 years from August 2025. In addition, the excise rebate for wine and beer will be increased from $350K to $400K.

No relief from announced but unenacted measures (ABUMs)

The instant asset write-off has not been extended. The previous budget announcement that extended the instant asset write-off to 30 June 2025 and the proposed non-deductibility of the general interest charge which is meant to apply from 1 July 2025 has not been passed by Parliament, with only one sitting day left before an election is likely to be called and Parliament is prorogued.

There are few announcements clarifying whether the long list of ABUMs will be actively pursued or whether part operative dates will be delayed.

- Last year’s budget announcement strengthening the foreign resident capital gains tax regime has had its start date delayed from 1 July 2025 to a date after royal assent.

- The 2023-24 budget announcement extending the clean building managed investment funds has also had its start date extended from 1 July 2024 to a date after royal assent.

- Tax agents, who having been wanting clarification about Division 7A, and corporate residency are still left in the dark.

Tax incentives

The government has expanded its Future Made in Australia policy to now allow production tax credits for green aluminum smelters that switch to renewable energy before 2036 as a cost of $2B over 19 years.

ATO compliance

Once again, rather than tax reform, the tax system is being asked to work harder. The Australian Taxation Office (ATO) has been provided with:

- $5.7M to enforce a ban on foreign residents purchasing existing dwellings

- $8.9M to implement an Audit and Compliance Program regarding foreign ownership of existing dwellings (along with Treasury)

- $717.8M for the Tax Avoidance Taskforce for 4 years targeting multinationals

- $155.5M for the Shadow Economy Compliance Program that focuses on worker exploitation, under-reporting of income, and illicit tobacco

- $4M illicit tobacco taskforce

- $75.7M Personal Income Tax Compliance Program for 4 years

- $50.0M Tax Integrity Program which focuses on timely payment of tax and superannuation by medium and large business.

Sanctions for tax agents

$27.4M has been provided to strengthen the sanctions available to the TPB, modernise the registrations framework and provide the TPB with funds to target high risk tax practitioners. With a start date of 1 July 2026 for sanction and 1 July 2027 for registration changes, the timeline for the detailed consultation about the proposals and then exposure draft legislation is extremely tight.

Some of the proposals are welcomed, such as:

- reintroducing criminal penalties for unregistered preparers

- introducing enforceable voluntary undertakings

- keeping the registered association pathway

- excluding the need for in-house tax advisers to register

- not pursuing the proposal to prescribe the ratio of individuals within an entity required to be registered practitioners

- modernising the registration process by introducing longer, alternative timeframes to gain relevant experience which assists those with career breaks

- not allowing micro credentials within primary qualification settings.

Others will need careful development, for example:

- enabling civil penalties to be imposed for Code breaches and increasing the civil penalties amounts

- introducing infringement notice penalties for alleged contraventions

- introducing interim and contingent suspensions

- requiring companies and partnerships to demonstrate appropriate governance arrangements

- requiring disclosure of spent convictions relevant to providing tax practitioner service.

CA ANZ will be working closely with Treasury and other industry bodies to ensure that these proposals are fit for purpose and are appropriate for various business sizes.

Proposals which have been discarded, such as not allowing micro credentials within secondary qualification settings and allowing the TPB to consider qualifications outside traditional tax practitioner courses of study should be reconsidered considering the shortage of tax practitioners.

Interestingly, the need for digital service providers to comply with the tax agent regulations when designing products that create tax outcomes is not mentioned.

Related download

Return to Federal Budget Coverage

Equipping you with the information and commentary you need to know about the Federal Budget.

Read more